India’s AI reckoning: The end of the labour-arbitrage era

The recent sell-off in technology stocks was treated by many as just another bout of market volatility. But instead of thinking of it as a random market panic, it shows something else.

In a matter of weeks, Indian IT companies lost nearly INR 6 lakh crore in market value. The Nifty IT index dropped more than 20 per cent, one of its sharpest corrections in decades. This was not triggered by a collapse in earnings. It was triggered by anxiety: AI is beginning to change the economics of the very model on which India’s IT industry was built.

For more than three decades, the IT services sector has been one of India’s greatest economic success stories. In FY 2024 — 25, exports touched roughly $224 billion. The sector contributes around 7 per cent to India’s GDP and employs close to six million people directly, with millions more indirectly dependent on it.

The model was straightforward and powerful. Indian firms offered skilled engineers at competitive cost. Global companies outsourced software development, maintenance, testing, and support to India because it was efficient, reliable, and scalable. Revenue was closely linked to effort — to billable hours. Time became money & AI started weakening that foundation.

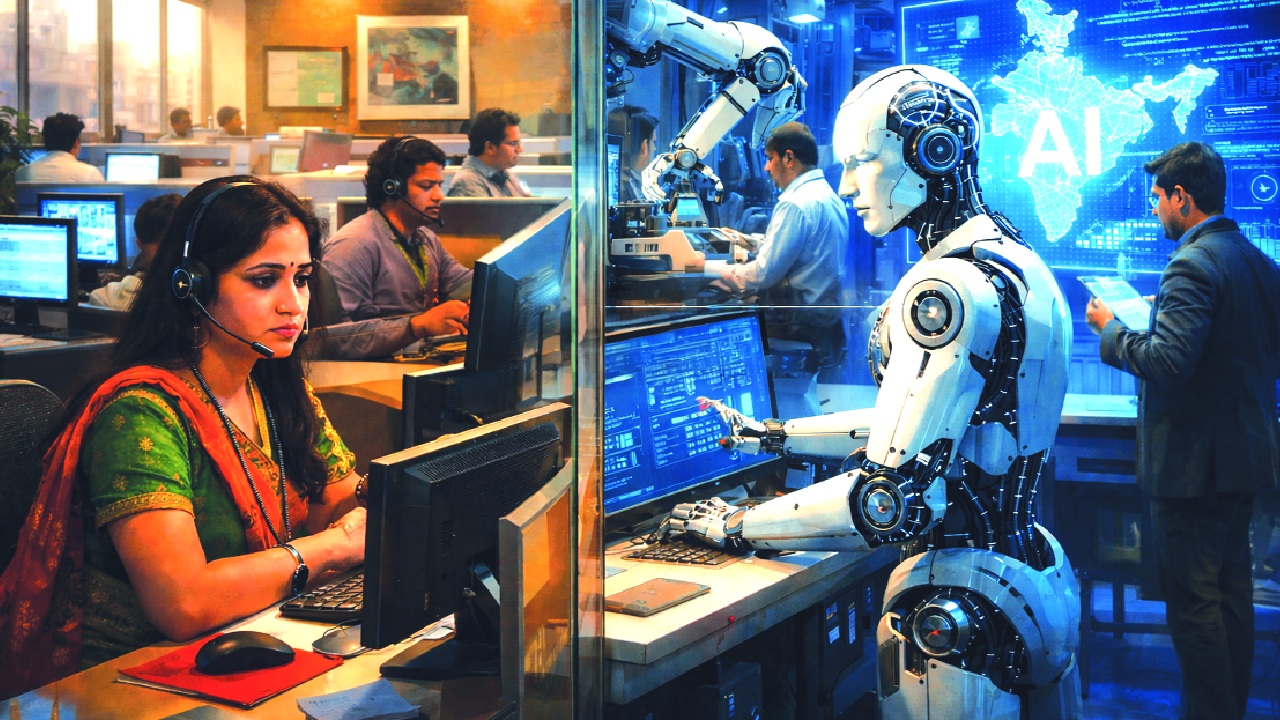

Modern AI tools can write code, catch errors, generate documentation, run tests, and assist in system design. Companies using these tools are reporting productivity improvements of 30 per cent to 40 per cent in certain tasks. A project that earlier required 10 engineers working for six months can now be completed faster and with fewer people. On the surface, higher productivity sounds like good news. And in many ways, it is. But for a sector that prices its services based largely on time and manpower, productivity gains create pressure.

If a client can complete the same work in fewer hours, why should they pay the same amount? Unless pricing shifts from hours to outcomes, revenue will compress. Even a structural reduction of 20 — 30 per cent in billable time across parts of the industry would have significant implications for export earnings over the next decade. This is what markets are beginning to price in. The concern is not that Indian engineers are becoming irrelevant. The concern is that the traditional labour-arbitrage model — where scale and cost advantage drive growth — may no longer deliver the same returns in an AI-assisted world. This matters for three reasons.

First, employment

India’s demographic dividend has long depended on the IT sector absorbing young engineering talent. Every year, hundreds of thousands of graduates look to technology firms for stable jobs and upward mobility. If automation reduces demand for entry-level coding, testing, and support roles, the impact may not be immediate layoffs. Instead, it may show up as slower hiring, fewer campus placements, and tighter margins for mid-level employees. At the same time, new opportunities will emerge. AI requires data engineers, model supervisors, cybersecurity experts, AI ethics specialists, and professionals who can integrate AI tools into business workflows. The key question is not whether jobs will disappear. It is whether India can retrain and reposition its workforce quickly enough. Countries that move fast on reskilling will benefit from AI. Those that delay will face structural unemployment in certain segments.

Second, competitiveness

Indian IT companies are not ignoring this shift. Leaders at major firms have publicly Stated that they are integrating AI across their operations. They understand that resisting automation is not an option. In fact, many are encouraging internal adoption even if it reduces short-term revenue. But adopting AI tools is not the same as owning AI platforms.

Today, the highest profits in the global AI ecosystem are being captured by companies that control foundational models, cloud infrastructure, and semiconductor design. These are capital-intensive areas dominated by the United States and, increasingly, China. Indian firms largely operate in the implementation layer — customising and deploying solutions built elsewhere. That role will remain important, but it carries thinner margins and less strategic leverage.

If India wants to capture more value from the AI economy, it must move up the stack. That means investing not just in services, but in intellectual property, proprietary platforms, and original research.

Third, strategic positioning

Artificial intelligence is not just another technology wave. It is becoming a layer embedded in finance, healthcare, defence, education, logistics, and governance. Countries that control AI capabilities will shape global standards, supply chains, and digital infrastructure.

India has demonstrated that it can build large-scale digital public infrastructure. Systems like Aadhaar and UPI show that population-scale platforms can be developed domestically and deployed efficiently.

The same ambition must now extend to AI. Currently, India depends heavily on foreign cloud providers and foreign-developed AI models. That is not unusual in a globalised world. But over-reliance can limit bargaining power and long-term competitiveness.

Building sovereign AI capacity does not mean isolation. It means ensuring that India has domestic research clusters, computing infrastructure, and data governance frameworks robust enough to support innovation at scale. There are positive signals. The Government has increased focus on AI policy discussions. International companies are investing in data centres and AI hubs in India. Domestic startups are emerging in sectors such as multilingual AI systems, agricultural analytics, and health diagnostics.

India’s diversity can also become an advantage. Training AI systems across hundreds of languages and dialects provides a testing ground that few countries can match. If properly supported, this could lead to globally competitive multilingual AI solutions. Yet optimism must be balanced with realism.

The global AI race is accelerating. The United States benefits from deep capital markets and dominant technology firms. China combines State coordination with industrial scale. Both are investing heavily in semiconductors, advanced computing hardware, and foundational research. India’s window of opportunity lies in combining its software expertise, demographic strength, and policy agility.

To do that, three shifts are essential. The industry must move from billing hours to billing outcomes. Clients will pay for measurable business impact — cost savings, efficiency gains, revenue growth — not just manpower. That requires new pricing models and deeper integration into client strategy.

The education system must adapt quickly. Engineering curricula should incorporate AI tools as standard practice, not electives. Continuous reskilling programs must become mainstream, supported by both Government and industry. And policy must focus on enabling infrastructure: affordable access to computing power, incentives for AI research, support for startups building foundational technologies, and clear regulatory guidelines that protect users without stifling innovation. None of this requires abandoning the services model overnight. The IT sector remains strong and globally respected. But relying solely on the old formula would be a strategic mistake. The recent market correction was a reminder that investors think in decades, not quarters. They are asking whether India’s technology sector will remain a cost-efficient service provider — or evolve into a creator of indispensable AI systems.

The difference between those two futures is not academic. It affects export earnings, job creation, currency stability, and national competitiveness.

India’s first IT revolution integrated the country into the global economy. The AI revolution demands a second transformation — from scale-driven growth to intelligence-driven growth. The opportunity is real. So is the risk. If India uses AI merely to work faster for foreign clients, the gains will be incremental. If it uses AI to build its own platforms, tools, and ecosystems, the gains could be transformative. This is not a moment for panic. It is a moment for clarity.

Markets have delivered their early warning. The question now is whether industry leaders, policymakers, and educators respond with incremental adjustments — or with structural ambition. India’s technology story has never been about fear of change. It has been about adapting faster than expected.

Artificial intelligence is the next test. How India responds will determine whether the country remains a crucial participant in the global digital economy — or becomes one of its architects. The shift has already begun. The only real uncertainty is the speed at which India chooses to move.

Author is a theoretical physicist at the University of North Carolina at Chapel Hill, US, and the author of the forthcoming book The Last Equation Before Silence; views are personal