Dirty dozen defaulters behind over Rs 5 lakh crore banking hole

For the past one month, The Pioneer reported a series on large defaulters of 11 PSU Banks and the three major private banks, based on the January and February filings of the banks to rating agency TransUnion CIBIL. Based on the data, we are publishing the details of the top 12 defaulters who plundered banks of more than Rs 5 lakh crore, out of more than Rs 29 lakh crore in dues from Large Defaulters.

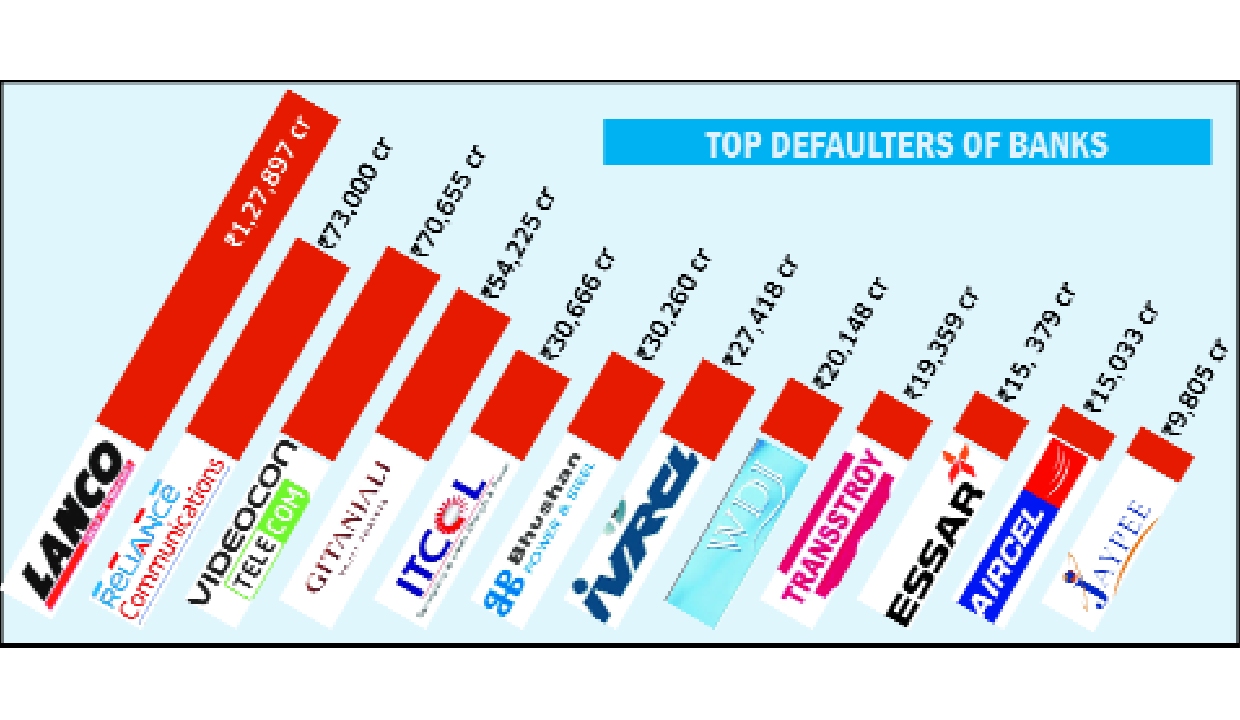

India’s top most defaulter is Lanco Group, headed by former Congress MP L Rajagopal, notorious for spraying pepper in Lok Sabha in February 2014, protesting against the bifurcation of Andhra Pradesh. Lanco Group and its power, steel and mining companies made a whopping default of Rs 1,27,897 crore to 10 banks. The banks filed only recovery cases against Lanco Group of companies and many of these companies are facing insolvency cases.

Union Bank of India, Punjab National Bank, Canara Bank, Bank of Baroda, Bank of Maharashtra, Central Bank of India, Bank of India, Punjab & Sindh Bank, ICICI Bank and Axis Bank are the lenders to the politically exposed Lanco Group, headed by Rajagopal. No bank has filed cases for bank frauds against promoter Rajagopal, who is nowadays parked in America and Australia, engaged in mining business. Many bankers say, due to his political clout loans were just allotted to his power, infra, mining projects till 2014 without any secure collaterals. They say, loans were diverted to abroad and no bank has filed cases against him or his companies for bank frauds.

Second top defaulter is Anil Ambani’s Reliance group of companies with big dues of Rs 71,433 crore to 12 banks. Anil Ambani’s companies started downfall from 2012 and banks were financing him till 2019. Few months ago, after Supreme Court’s direction, Banks have registered cases against him for bank frauds and Enforcement Directorate informed that his total bank loan dues have crossed more than Rs 73,000 crore.

Recently Anil Ambani wrote to Finance Minister Nirmala Sitharaman to grant him bailout package, citing Government’s bailout package to controversial Sandesara Group. In November 2025, Central Government allowed then fugitives, now respected Sandesara brothers Nitin and Chetan Sandesaras to settle all their dues of more than Rs 19,000 crore by paying Rs 5,100 crore only. Supreme Court approved on Central Government’s bailout package, which allowed quashing of all criminal cases including bribing Income Tax officers and creation of fake Albanian passports to flood the country.

Third top defaulter is tainted Videocon Group headed by Venugopal Dhoot and his brother former Shiv Sena MP Rajkumar Dhoot. As per the TransUnion CIBIL data, this politically exposed group owes Rs 70,655 crore to seven banks. The seven banks plundered by Videocon group are: Central Bank of India (Rs 25,299 crore), SBI (Rs 23,296 crore), Bank of India — Rs 9,606 crore), Bank of Maharashtra (Rs 6,722 crore), Bank of Baroda (Rs 5,296 crore), Indian Overseas Bank and UCO Bank.

Interestingly, ICICI Bank has not shown the dues of Videocon Group. Venugopal Dhoot was arrested by CBI for bribing ICICI Bank head Chanda Kochhar. In 2018, it was exposed that ICICI Bank allotted Rs 3250 crore to Videocon and bribery of 10 percent was diverted to Chanda Kochhar’s husband Deepak Kochhar’s companies. In TransUnion CIBIL data of large defaulters up to February 2026, name of Videocon is not seen in ICICI Bank’s filing. Previous week only SBI approached NCLT against the Dhoot brothers to materialise their personal guarantee of around Rs 10,000 crore.

The banks are also silent about allotting more than Rs 40,000 crore to Videocon Group’s oil project in Mozambique in 2012. ICICI Bank was the lead banker in Videocon’s Mozambique oil exploration project, along with many PSU Banks. In 2017, Videocon Group sold 10 per cent of share of the oil exploration company to ONGC for Rs 2.47 Billion Dollars and made a huge profit, while not repaying their loans. Why Banks and Government were silent in catching Dhoot brothers is still a mystery, when they got huge bonanza?

Fourth top defaulter is fugitives Mehul Choksi and his nephew Nirav Modi headed firms Gitanjali Gems, Nakshtra World, Firestar Diamonds and Gitanjali Exports. Till 2018, these guys were holly cows. Nine banks - Punjab National Bank, Union Bank, SBI, Canara Bank, Bank of Maharashtra, Central Bank, UCO Bank, Punjab and Sind Bank and ICICI Bank — were given Rs 54,225 crore to these fugitives.

Other top defaulters are Himachal Pradesh based, Delhi registered company facing insolvency Indian Technomac (Rs 30,666 crore), fizzled out Bhushan Power & Steel (Rs 30,260 crore), Hyderabad based IVRCL Ltd (Rs 27,418 crore) and fugitive Jatin Mehta’s Winsome Diamonds (Rs 20,148 crore). All these companies are facing insolvency or at the liquidation stage and ultimately banks have to write off their loans, as banks have no secure collateral securities, when providing huge loan amounts. Banks only have pledged shares of these companies and personal guarantees of directors of these companies. The shares have no value after insolvency cases and promoters have parked their assets safely in abroad and other directors are only employees, having no big assets. Many Bankers vouch all these huge loans were given out of political pressures.

Another interesting big defaulter is a Russian company named Transstroy India Ltd, facing recovery of Rs 19,359 crore from four PSU Banks — Union Bank of India, Bank of Maharashtra, Central Bank of India, UCO Bank and Bank of India. This Guntur-based company is headed by long-term Guntur’s Congress-turned-TDP vociferous MP Rayapati Sambasiva Rao. In 2018, CBI and Serious Frauds Investigation Office (SFIO) found that funds were diverted through shell companies created in the names of employees, including his cooks, maids, drivers and sweepers.

This company and its more than 50 subsidiaries are engaged in road construction, toll plaza operations, rail, and power contracts is now facing CBI and ED cases. Interestingly, the Central Bank has given loan to Transtroy India’s linked company, Betul Tollways Private Limited and a Russian Citizen Oleg Sergeev, is shown as personal guarantor. This person is director of many toll companies of Sambasiva Rao.

Collapsed Essar Group of Ruia brothers owes Rs 15,379 crore to Union Bank, Central Bank and UCO Bank. Fugitive C Sivasankaran’s Aircel Mobile, Dishnet Wireless and Sterling Group plundered Rs 15,033 crores of four PSU banks — SBI, Canara Bank, Central Bank and Union Bank. DMK supported Sivasankaran, now settled in Seychelles Island was plundering PSU banks up to 2010, till 2G Scam broke out.

Uttar Pradesh’s big real estate company Jaypee Group owes Rs 9,805 crore to four banks — ICICI Bank, Axis Bank, UCO Bank and Punjab & Sind Bank. Now Gautam Adani and Vedanta’s Anil Agarwal are engaged in bitter battle to acquire insolvent Jaypee Group, leaving banks on how to acquire their dues. Other major top defaulters are collapsed real estate firms Zoom Developers (Rs 8314 crore) and Supertech (Rs 6213 crore).

Another top defaulter is a real estate firm in Delhi, UP, Haryana, Punjab, based Era Group with dues of Rs 5,063 crore to Canara bank, UCO Bank, Indian Overseas Bank and Punjab & Sind Bank. The Pioneer on March 12, 2026, edition, highlighted that Union Bank of India tops among the largest defaulters with Rs 9.96 lakh crore with 18,197 cases or entries as per the Bank’s own filing to rating agency TransUnion CIBIL up to January 2026. The large defaulters list means those who owe more than Rs One crore and above to a bank, and the bank is conducting recovery cases against them. As per Union Bank’s filings, their largest defaulter is Hem Singh Bharana-controlled Era Group with dues of Rs 75,714 crore.

The Pioneer emailed Union Bank of India’s MD and CEO, Asheesh Pandey, and his colleagues on April 1, asking how the alteration/reduction had occurred in their filings to TransUnion CIBIL in February, reducing Rs 9.96 lakh crores to Rs 4.93 lakh crores within a month. Till the time of going to press, The Pioneer did not received any response.

The basic questions raised by The Pioneer was — “We have seen your latest report to TransUnion CIBIL after The Pioneer’s expose, which reduced from Rs 9.96 lakh crores to Rs 4.93 lakh crores dues in large defaulters list. We are not going into the specifics of each loan. We have a specific question: According to your January 2026 list, Era Infra Engineering (Era Group, headed by Hem Singh Bharana) was your largest defaulter with more than Rs 75,000 crores. In your new list of February 2026, submitted to TransUnion CIBIL, this name is not included. Has he paid dues, or have you allowed a one-time settlement, or have you written off the loans or have you re-structured the loans?”

And interestingly, a PSU Bank - Indian Bank has not filed their Large Defaulters List to any rating agency approved by the Reserve Bank of India for the past one year. India has now 12 PSU Banks and except Indian Bank, all Banks are providing data of large defaulters to RBI approved rating agencies on monthly wise. Why Union Bank not giving their list of Large Defaulters? Finance Ministry must direct Indian Bank to publish their Wilful Defaulter and Large Defaulter List. Indian Bank was involved in many scams and its’ Chairman of M Gopalakrishnan (passed away in 2016) was in jail for many years for big loan frauds in mid 90s, approving from Five Star Hotels in Chennai. Indian Bank, which carries such bad legacy, for the past one year, not yet uploaded their Wilful Defaulter and Large Defaulter List to TransUnion CIBIL.

The Finance Ministry must take immediate cognisance of the glaring lapse by Indian Bank in failing to upload critical data, even as all other public sector banks adhere to the mandated monthly disclosures. Such inconsistency raises serious concerns about transparency, accountability, and possible attempts to obscure irregularities. The Ministry, in coordination with the RBI, must initiate a time-bound inquiry to ascertain the reasons behind this non-compliance.

More importantly, this episode underscores the urgent need to confront the deeper malaise afflicting the banking system, a troubling nexus between wilful defaulters, sections of bank management, regulatory blind spots, and influential elites. This nexus has eroded institutional credibility and weakened the very foundation of financial governance.

Strict and exemplary action must follow. Authorities should not hesitate to order independent forensic audits, reopen suspicious accounts, and launch fresh criminal investigations wherever collusion is suspected. Accountability must extend across the chain-bank officials, corporate defaulters, and any external actors found complicit. Regulatory oversight mechanisms must also be reviewed and strengthened to prevent such lapses from recurring.

Restoring public trust in the banking system requires more than rhetoric; it demands decisive enforcement, institutional integrity, and zero tolerance for collusion and concealment.

Leave a Comment

Comments (2)

Wow nice article. These thug’s getting away and common man is being harassed by CIBIL scores if he defaults by 1000 rupees.

PSU banks are easy target for corporate houses with political backing regardless of who is in power at center.The rehtorics by PM and FM about mobile banking continues even in 12 yrs of NDA rule if one go by data provided in article.