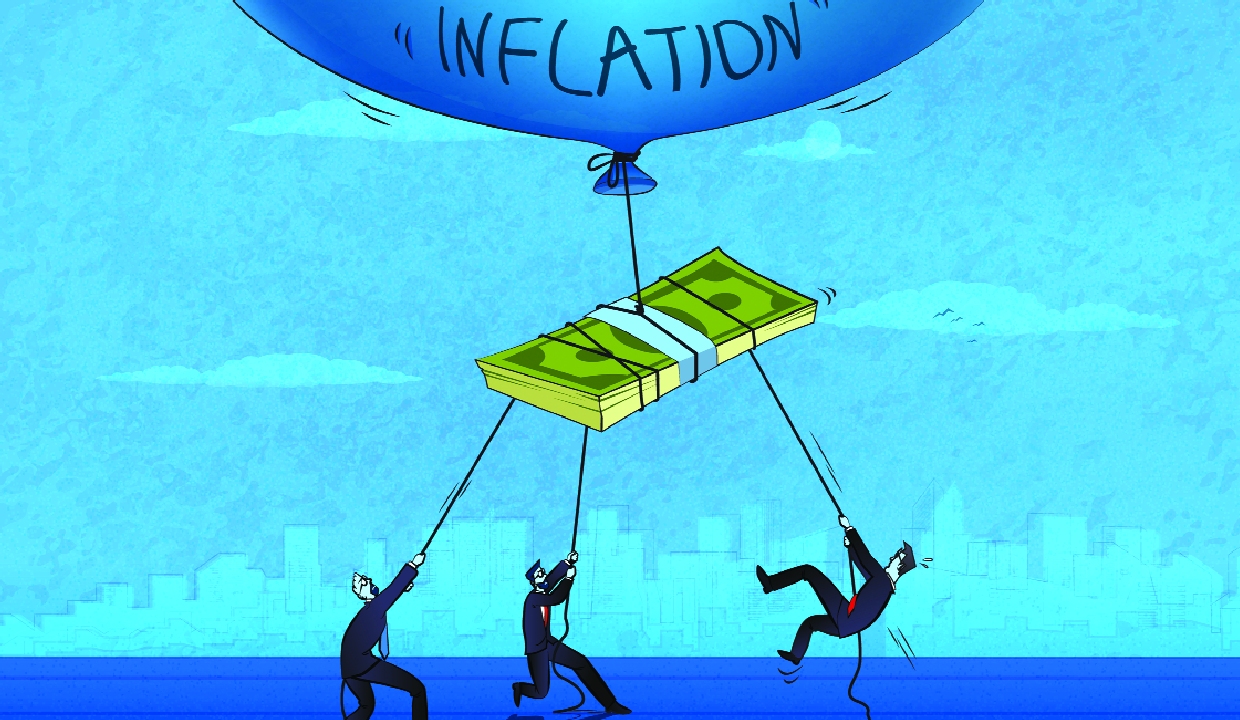

Cost of inflation on investments

If inflation returns, will retail investors earn better returns?

For most Indian retail investors, except for the damaging interlude in 2026, and possibly earlier, the past few years seemed rewarding. Portfolio values rose, equity markets delivered strong gains until 2026, and the first several months in 2025, and fixed-income instruments offered stable returns. But as equities wobble, portfolios are cobbled afresh, people are doubled under the strain of uncertain interest rates, and troublesome inflation may flare up again, a deeper question emerges. How will the investors create wealth to beat inflation, or to keep up with it? It is time to calculate the costs of price rises on returns.

With the ongoing global tensions, although there are signs of an Iran-US ceasefire due to the ongoing peace talks, elevated global crude oil prices, and currency pressures, inflation is a key concern. The World Bank projected India’s retail inflation at 4.9 per cent for the current year, which is higher than the Indian central bank’s figure. Yet, both estimates agree that prices will be influenced largely by higher food and energy costs, along with the exchange rate pressures. While an inflation under five per cent does not seem unduly alarming, even moderate by the past benchmarks, the impact on returns is significant.

Like it or not, believe it or not, inflation quietly but surely erodes a household’s purchasing power, and drives down the returns on savings and investments. Despite the seemingly-positive earnings, the real gains, after adjusting for inflation, are lower than what they appear. For example, if a fixed deposit offers an annual return of 6-7 per cent, and inflation is at 4.9 per cent, the actual return is barely 1-2 per cent. Deduct the applicable taxes on the earnings, and the figure dwindles further. Nominal growth in savings is impacted by realities.

Hence, while the investors feel good about the nominal, or overall, returns, they realise that what they are left with after accounting for the price rises is minimal. Logically, the ability to spend does not improve, and even to maintain lifestyles seems tough. This gap is particularly important for retirees, and conservative investors who rely heavily on fixed-income products. Instruments such as FDs, debt funds, and small savings schemes struggle to consistently deliver inflation-beating returns. Investors struggle with budgets, and expenses. Inflation has the ability to upset the investment-savings apple cart.

Of course, we need to first figure out why inflation is on the rise, after it slumped, with food inflation in the negative (yes, prices actually came down). The current pressures are driven by a combination of global and domestic factors. Rising crude oil prices are a key contributor, especially for an import-dependent country like India. Geopolitical tensions further disrupt the global supply chains, and increase volatility in the commodity markets. At the same time, a weakened rupee makes imports more expensive, which adds to the price rises.

Equity investors may be relatively better positioned in an inflationary environment. Over the long term, equities have outpaced inflation, and delivered real positive returns. Firms often pass on the rising costs to the consumers to protect margins and earnings. But this is a tricky area. Inflation counts when equities are depressed, or extremely volatile, as is the case now. This year, the Sensex, the Bombay Stock Exchange Index, lost 7,000 points, or more than eight per cent. In addition, price rises, especially when the estimates go beyond the benchmarks set by the central bank, may lead to higher interest rates, tighter monetary policy, and lower stock valuations.

As is the case now, the fears of inflation, coupled with the expectations of lower GDP growth can trigger market volatility. For the retail investors, this implies that while equities remain a key tool to create wealth, short-term returns are uneven. It is difficult to stay invested in such situations, despite the knowledge that the real benefits of equities lie in hanging there over longer periods rather than reacting to near-term market movements. Fixed-return instruments may gain due to the higher interest in such scenarios but, as mentioned earlier, the higher gains are immediately eroded by the higher inflation.

This explains why the focus during periods of price rises invariably falls on the debt and fixed-income investments. Traditional options such as FDs, bonds, and debt mutual funds deliver returns that are often unable to keep pace with inflation, especially after accounting for taxes. This creates a dilemma for the risk-averse conservative investors, especially the retirees. While these choices offer safety, security, and predictability, they may not help to preserve wealth over time. Those who rely solely on fixed income, and there are a lot of them despite the advice to diversify portfolios, may find that their savings are effectively losing value in real terms, even if the nominal figures are stable.

The key takeaway for the retail investors in such a scenario is to focus on real returns, and not just nominal gains. It is not an easy task, especially for those who swear by FDs, bonds, and debt funds. It is essentially to expand the portfolios, and go for a balanced mix that reflects the risk-averseness and safety issues. Equities should play a role to achieve long-term growth, while debt instruments can stay to provide stability and liquidity. Yet, the mix is tricky. Different experts, given their penchant for risks, advice differently.

For example, some contend that 50 per cent needs to be stocks, 35-40 per cent debt, and rest in gold and others. Others talk about 60-70 per cent in debt, and 20-25 per cent in equities. It is a choice that each individual needs to make. However, hybrid funds, inflation-linked strategies, and systematic investment plans (SIPs) can balance the risks and returns. It is crucial to periodically review investments, and adjust the allocations based on changing economic conditions. Hence, the 50:40 equity-debt ratio may change to 25:70, or vice versa. One cannot stick to a ratio, or depend only on fixed-income options.

Always remember, the reach of the tentacles of inflation are not always visible, but their grasp and clutches are forceful. In the current scenario, with expectations of lower growth and higher inflation over the next 1-2 years, and rising global uncertainty, the retail investors need to look beyond the headline returns, and assess whether their portfolios and investments are truly growing in real terms. The fact remains that in the end, it is not just about how much your portfolio grows but how much it actually buys, and allows to maintain lifestyles.